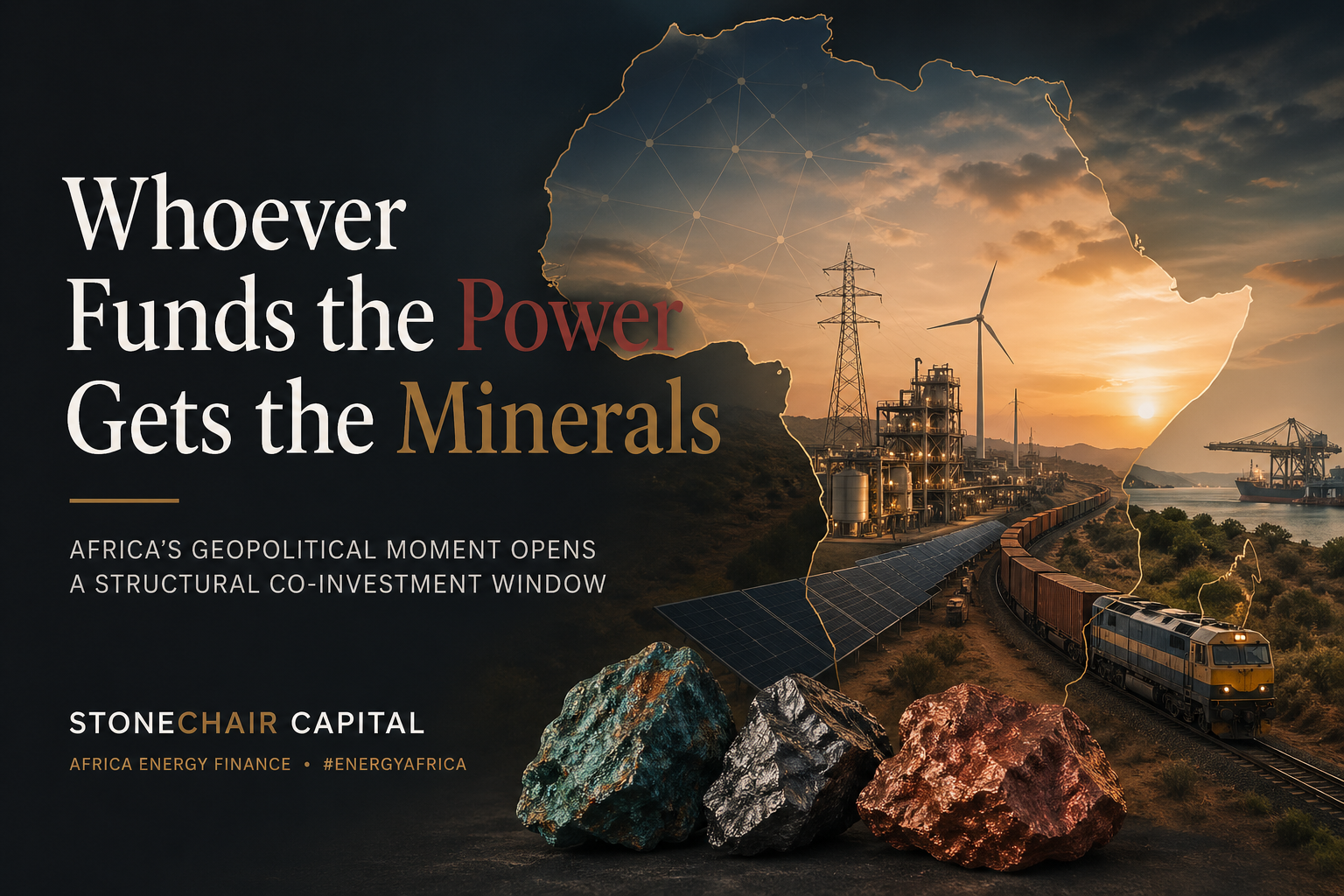

Whoever Funds the Power Gets the Minerals

Whoever Funds the Power Gets the Minerals: Africa’s Geopolitical Moment Opens a Structural Co-Investment Window

Africa Has Found Its Leverage

In February 2025, the Democratic Republic of Congo imposed a blanket ban on cobalt exports. Prices, which had collapsed to multi-year lows near $22,000 per tonne, were undermining the economics of an industry that supplies approximately 75% of global cobalt output (S&P Global). By October 2025, Kinshasa replaced the ban with a structured quota regime—capped at 18,125 metric tons for the remainder of 2025 and 96,600 tons annually through 2027—and cobalt prices rallied ~170%, recovering to approximately $54,000–$55,000 per tonne (Benchmark Minerals, Africanews).

President Tshisekedi’s framing was explicit: the export controls were “a real lever to influence this strategic market” after years of what he characterized as predatory pricing by international buyers. Whether one accepts that framing or not, the market outcome was unambiguous. The DRC used its supply concentration to reprice the global cobalt curve. That is not a coincidence—it is a policy template now being studied and replicated across the continent.

More than a dozen African nations have implemented export restrictions or outright bans on raw mineral shipments to promote in-country beneficiation. The G20 Critical Minerals Framework, adopted at the 2025 Johannesburg Summit under South Africa’s presidency, institutionalized this direction at a multilateral level, explicitly calling for African nations to capture more value from their mineral endowments before export.

Africa holds approximately 30% of the world’s critical mineral reserves, yet currently earns only a fraction of their processed value—continental extraction generated roughly $50 billion in 2024, while refining generated only $16 billion.

The Great Power Contest Is Deploying Real Capital

The United States, European Union, and China are each treating African mineral access as a strategic priority—and deploying financing accordingly. China’s state-owned enterprises dominate over 70% of global cobalt and lithium refining capacity and are deepening their presence in DRC mine operations, the Tanzania-Zambia rail corridor, and downstream processing across the continent.

The Western response is structural and accelerating. The G7’s Partnership for Global Infrastructure and Investment has committed to mobilizing up to $600 billion by 2027, with Africa as a primary focus.

The Lobito Corridor—a rehabilitated rail link connecting the DRC Copperbelt and Zambia to Angola’s Atlantic port—has attracted global commitments exceeding $6 billion, anchored by a $553 million loan from the U.S. International Development Finance Corporation and an EU pledge of over €2 billion for energy, transport, water, and mining across the Zambian corridor segment.

The Entry Point: Energy Infrastructure Behind Sovereign Capital

Here is where the investment thesis sharpens. DFI capital is securing the macro framework, but the energy and processing infrastructure required to translate mineral extraction into value-added exports remains critically underfunded.

The energy constraint is severe. In the DRC, the world’s largest miners—Glencore, Ivanhoe, CMOC, Zijin—collectively spend an estimated $600 million per year on diesel generation because grid power is unavailable at industrial scale.

In Zambia, mining consumes 51% of national electricity supply, and drought-driven declines at Kariba Dam have produced power cuts of up to 21 hours per day, directly causing the shelving of a planned nickel refinery.

Processing minerals in Africa—rather than exporting raw ore to Chinese refineries—would create an estimated 2.3 million jobs and increase continental GDP by approximately 12%. That ambition is not achievable without a parallel energy buildout. No smelter runs on ambition.

The investment structure that closes this gap is well established: captive mine-site power generation—solar, run-of-river hydro, gas-to-power—structured as project finance with long-term PPAs signed directly by mining companies.

The Window Is Now

Geopolitical competition for African critical minerals is not a future risk—it is a present capital allocation reality. The US, EU, and China have each established financing positions, and competitive dynamics are forcing concession terms that favor in-country value addition.

Stonechair Capital’s focus is the enabling layer: African energy infrastructure that de-risks mineral value chains, improves access to growth capital, and creates investable platforms for future institutional capital.

The minerals are African. The leverage is now African. The capital required to unlock the full value chain is still seeking deployment. In this cycle, control of energy infrastructure will define control of the mineral value chain.

Sources & References

- DRC cobalt export quotas to support cobalt prices — S&P Global Market Intelligence

- DRC to lift cobalt export ban and impose quotas through 2027 — Benchmark Minerals

- DRC resumes cobalt exports after 10-month ban — Africanews

- Critical minerals geopolitics in 2026 — ODI

- Competing for Africa’s Resources — Stimson Center

- Global commitments to the Lobito Corridor surpass $6B — Energy Capital & Power

- DFC signs $553M loan agreement for Lobito Atlantic Railway — DFC

- Modernizing Africa’s Lobito Railway — Columbia CGEP

- Southern Africa’s critical minerals — World Economic Forum

- Africa at the Core of Critical Minerals — B20 South Africa