East Africa E-Mobility: Policy Divergence and Investment Implications

East Africa E-Mobility: Policy Divergence and Investment Implications

The Fiscal Logic Behind Electrification

Ethiopia’s prohibition on new gasoline and diesel vehicle imports illustrates the fiscal pressures driving transport electrification across East Africa.

With fuel import costs approaching $4.2 billion annually and monthly subsidy obligations of approximately $128 million, the policy decision was driven primarily by balance-of-payments constraints rather than climate commitments.

The sequencing matters: Ethiopia’s EV transition was demand-led by government intervention, not market-led by consumer preference.

Fuel imports are dollar-denominated, creating structural currency exposure for governments and operators alike. Commercial motorcycle operators — the largest segment of the regional EV market by unit volume — base adoption decisions on daily operating costs.

At current fuel price levels, the economics of electric two-wheelers are compelling for high-utilisation operators, independent of any policy incentive.

Regional Market Scale

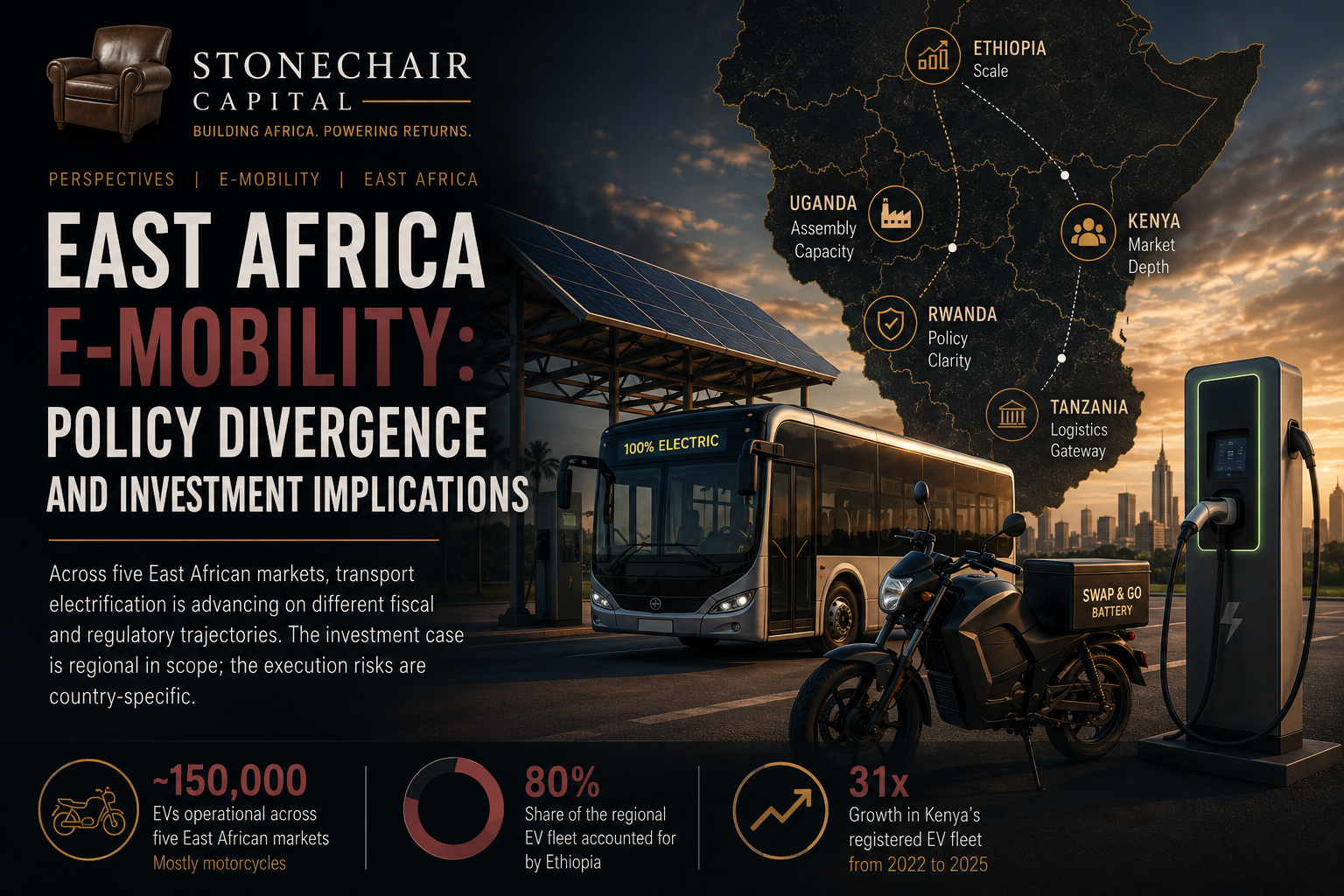

As of mid-2026, approximately 150,000 EVs are operational across Kenya, Ethiopia, Rwanda, Uganda, and Tanzania, the majority motorcycles.

Ethiopia accounts for approximately 80% of the regional fleet.

Kenya’s registered EV fleet grew 31× from 796 vehicles in 2022 to 24,754 in 2025.

The regional market remains concentrated in motorcycles, battery-swapping, and commercial fleet deployment.

The central question for investors is not whether the market will grow, but whether national fiscal and regulatory frameworks will provide sufficient stability to support project-level financing.

Ethiopia: Fiscal Necessity as Policy Driver

Ethiopia’s EV adoption trajectory reflects the interaction between fiscal necessity and direct policy intervention.

The government’s decision to prohibit combustion vehicle imports was preceded by sustained pressure on foreign exchange reserves and an annual fuel import bill that the domestic subsidy framework could not sustain.

The measure was a balance-of-payments response, not a climate initiative, and should be evaluated as such.

The resulting fleet — estimated at over 115,000 vehicles — is the largest in sub-Saharan Africa outside South Africa.

However, the pace of fleet growth has outrun the supporting infrastructure. Charging capacity, grid reliability at key commercial nodes, and battery logistics remain underdeveloped relative to fleet size.

Uganda: Industrial Policy and Cost Structure

Uganda offers a useful precedent for evaluating incentive-dependent investment theses.

The government introduced a zero-duty period on EV imports consistent with its 2023 National E-Mobility Strategy, then reversed that position by reinstating a 25% import duty on EVs, hybrids, and electric motorcycles.

The reversal reflected a preference for domestic assembly capacity over near-term imported vehicle adoption.

The underlying industrial policy rationale is not without merit. Local assembly develops supply chain depth, reduces long-term import dependency, and retains more value-add within the domestic economy.

However, the near-term effect is a material increase in the landed cost of imported EVs, directly constraining operator adoption rates in a market where affordability remains the primary barrier.

Rwanda and Kenya: Clarity vs Scale

Rwanda maintains the most clearly structured incentive regime in the region.

The Rwanda Revenue Authority has confirmed 0% import duty on electric and hybrid vehicles and electric motorcycles through at least June 2028.

The defined policy horizon reduces one class of uncertainty that remains prevalent elsewhere in the corridor.

Kenya presents a different profile. Registered EV fleet growth from 796 vehicles in 2022 to 24,754 in 2025 demonstrates substantial commercial demand concentrated in motorcycles, fleet operators, and urban transit.

Kenya also possesses the deepest private-sector EV ecosystem in the corridor outside Ethiopia.

The principal near-term risk is fiscal. As electrification reduces fuel consumption, excise revenue declines. A proposed 16% VAT on EVs remains under active consideration.

Capital Allocation: Where the Opportunity Sits

The near-term investment opportunity in East African e-mobility is concentrated in commercial and infrastructure segments rather than private vehicles.

Commercial two-wheeler operators represent the largest addressable market by unit volume. The operating cost advantage of electric motorcycles over petrol equivalents is now sufficiently established that adoption is increasingly driven by economics rather than subsidy.

Battery-swapping infrastructure is emerging as one of the most important enabling layers in the market. By decoupling battery ownership from vehicle ownership, operators reduce upfront vehicle cost while creating recurring contracted revenue streams for network operators.

Urban electric bus systems in Nairobi, Kigali, and Addis Ababa are progressing through procurement and pilot deployment stages, although bankability remains highly dependent on counterparty credit quality and depot-level grid reliability.

Local assembly presents a differentiated opportunity for investors with longer time horizons and appetite for manufacturing risk, particularly in Uganda and Kenya where policy support is more explicit.

Investment Implications

The structural drivers of East African transport electrification — dollar-denominated fuel costs, operator sensitivity to daily operating expenses, and government pressure to reduce energy import dependency — are sufficiently entrenched that the direction of the thesis is not in question.

The relevant risk is to the pace and predictability of the policy environment, not to the underlying demand trajectory.

Stonechair Capital’s diligence framework for this market is organised around five policy-level questions:

• Is the government’s objective to accelerate imported EV adoption or develop local assembly capacity?

• Are charging equipment and batteries classified as productive infrastructure or consumer imports?

• Are incentives statutory with defined review timelines, or discretionary?

• How does the government intend to replace declining fuel excise revenue?

• Is the EAC making measurable progress toward harmonised tariff codes, standards, and charging frameworks?

Several policy-level inflection points are likely to resolve within the next 12–24 months. Rwanda’s 0% duty regime is subject to review ahead of its June 2028 expiry. Kenya’s proposed VAT framework remains active. Uganda’s assembly framework is still evolving. Tanzania’s draft EV framework remains under consultation.

Each represents both a potential catalyst and a source of downside risk depending on the policy outcome.

Investors seeking exposure to the corridor should structure positions and partnership agreements with sufficient flexibility to accommodate policy revision, while weighting Rwanda and Kenya disproportionately in initial deployment given the relative clarity of their current frameworks.

This article is prepared by Stonechair Capital for informational purposes only and does not constitute investment advice or a solicitation to buy or sell any security. Past performance is not indicative of future results.