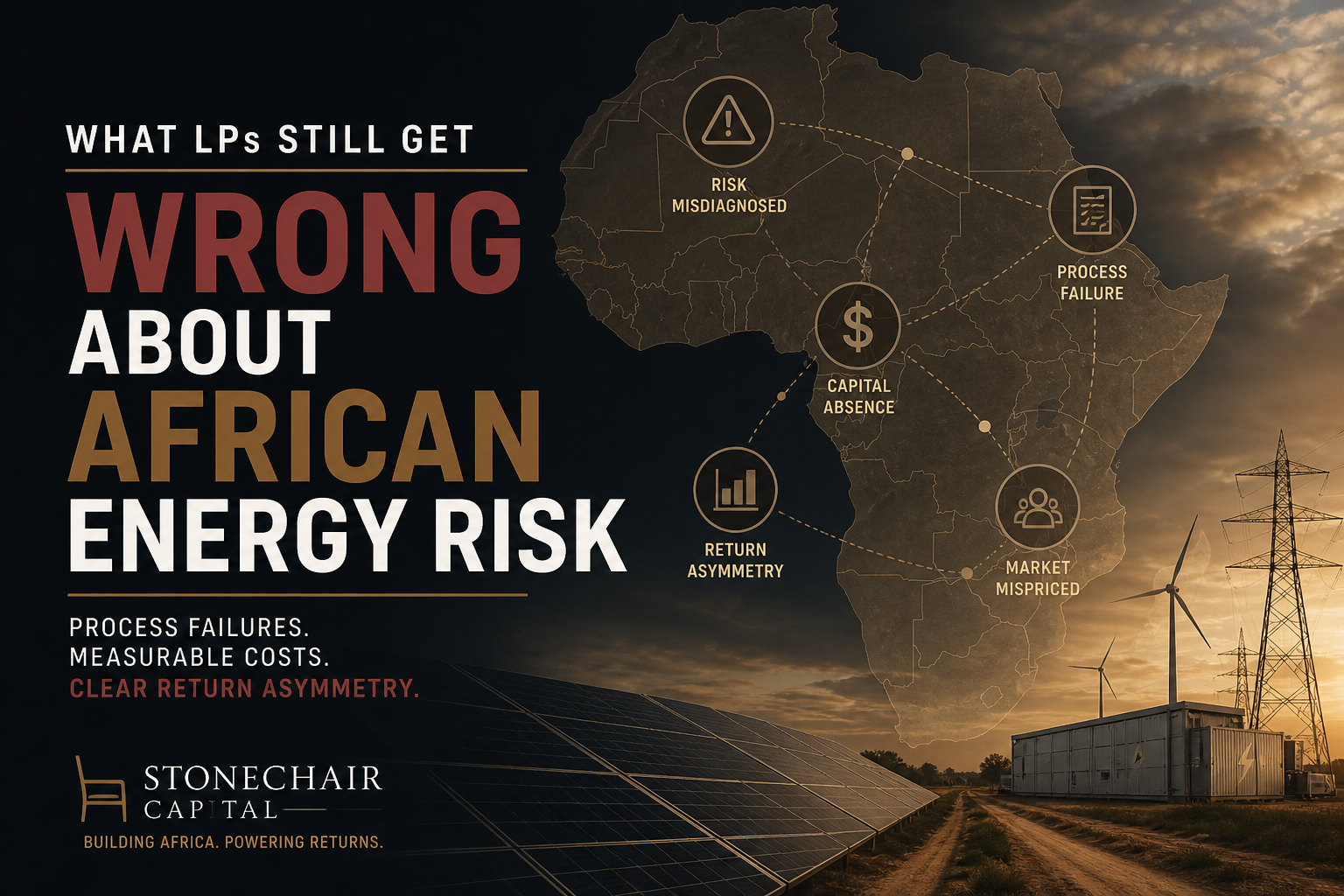

What LPs Still Get Wrong About African Energy Risk

What LPs Still Get Wrong About African Energy Risk

Hiding Behind “Mandate Constraints”

Ask any pension fund or insurance allocator why they are not active in African energy and the answer is predictable: “It falls outside our mandate.”

This is rarely true.

Most mandates do not prohibit African exposure. They prohibit poorly rated assets, unhedged currency exposure, or structures outside predefined thresholds.

Outsourcing Thinking to Consultants

Most LP decisions are shaped before they reach the investment committee.

Consultants, asset allocation models, and benchmark frameworks determine what is “investable.” Africa fails those filters — not because of returns, but because it does not fit the model. It sits outside indices. It lacks standardized datasets. It carries rating penalties that automatically push it into high-risk buckets.

So it is excluded. This is not portfolio construction. It is model compliance.

Treating Ratings as Investment Policy

Only two African sovereigns — Botswana and Mauritius — carry investment-grade ratings. For many LPs, that ends the discussion.

It should not.

Infrastructure investors routinely take project-level risk in developed markets that exceeds sovereign risk. They rely on structuring, contracts, and cash flow visibility. In Africa, the same logic is abandoned because a sovereign label triggers a stop.

This is not discipline. It is inconsistency.

Leaving Return on the Table

African infrastructure clears at materially higher yields than comparable assets with similar fundamentals. The spread is persistent — roughly 150 basis points or more in many cases.

LPs interpret that as compensation for risk. It is not.

Financing a solar project in Kenya or Senegal costs 8.5–9%, while an equivalent project in Europe or North America prices at 5–6%. An identical solar installation in Nigeria costs three times more to finance than one in Madrid — not because the technology differs, not because the sun shines less, but because of structural biases in ratings and a persistent absence of competing capital.

Absence, by definition, is correctable.

Misdiagnosing Currency Risk

Currency risk is cited as the primary barrier. In reality, it is the least understood variable in the stack.

Volatility exists. Between 2014 and 2024, the Nigerian naira depreciated over 800% against the US dollar. The Ghanaian cedi lost over 280%. These are real numbers. But exposure is driven by structure, not geography.

The underlying problem is a mismatch embedded in conventional project finance: hard-currency debt against local-currency revenue. When a state utility offtaker pays an IPP in local currency but that IPP services USD-denominated debt, currency movement becomes a structural crisis. That fragility can be mitigated, hedged, or designed out entirely.

Operators in the East African market are already solving for it through different routes. Traditional IPPs like East African Power — a Kigali-based hydro and solar developer with 18 projects and $60 million in deployed CAPEX — structure carefully around local-currency PPA offtake. EaaS operators like Powerhive collect revenue directly from end-users in local currency by design, removing the utility mismatch at the project level entirely.

LPs are not rejecting currency risk. They are rejecting the work required to engage with it.

Ignoring Blended Structures

Blended finance is dismissed as non-core. That is incorrect.

It is a mechanism to make assets investable within institutional constraints. First-loss capital absorbs downside. Guarantees reshape credit profiles. Senior tranches become eligible for institutional capital at risk-adjusted returns that mandates can accommodate.

The Scatec 1.1 GW solar-plus-storage project in Egypt demonstrates the model: nearly $480 million structured with British International Investment, the African Development Bank, and the EBRD — concessional capital enabling commercial capital to occupy the senior tranche. GuarantCo’s credit guarantee instruments work the same way, converting project exposure into investment-grade-equivalent structures that pension funds and insurance companies can deploy against mandates they already hold.

LPs that exclude blended structures are excluding the market.

Allocating to Comfort, Not to Opportunity

Africa receives roughly 1.5% of global clean energy investment. Compare that to how LP portfolios are actually constructed:

Emerging markets target — global infrastructure allocations: 10–15%

Energy transition share — new infrastructure deployment in developed markets: 30–50%

Historical early-cycle allocation — high-growth underpenetrated markets: >20%

Actual LP exposure — Sub-Saharan African energy, typical: <1%

Africa’s share of global clean energy investment: 1.5%

Africa meets all three benchmark criteria: emerging market, energy transition opportunity, structural supply-demand gap.

This is not underweight. This is absence.

The Decision LPs Actually Face

This is not an abstract debate. It is a timing issue.

The repricing has started. Middle East instability is disrupting approximately 20% of global oil and gas trade. Investors carrying implicit assumptions about Gulf energy reliability are being forced to reconsider. In that context, Africa’s relative insulation from major global conflict — combined with improving regulatory frameworks across key markets — is repositioning the continent as a strategic capital destination.

Africa does not need to become low-risk. It only needs to become relatively more attractive than the alternatives.

That is already happening.

The Call to Action

LPs now have three options.

Build direct exposure. Develop internal underwriting capability. Engage at the project and structure level. Accept that this is not a benchmark-driven allocation.

This is where structural mispricing is captured.

Access the market through managers and platforms with existing expertise. This reduces execution risk and accelerates entry.

Returns compress. Access remains.

Follow the default path. Wait for consultants to adjust frameworks. Wait for rating agencies to recalibrate. Wait for Africa to fit neatly into institutional models.

By that point, pricing will reflect reality. Returns will not.

The real risk is being late.

This article is for informational purposes only and does not constitute investment advice or a solicitation to buy or sell any security.